Risk Partners Life Sciences Roundtable 2025, thank you very much!

Auf einen Blick:

Die Contingent Risk Insurance ist relevant, wenn ein bekanntes Einzelrisiko eine Transaktion, Finanzierung, Bilanzposition, Ausschüttung oder Verhandlung belastet, sein Ausgang aber noch offen ist. Typische Fälle sind behördliche Rückforderungen, regulatorische Unsicherheiten, verwaltungsrechtliche Verfahren, drohende oder laufende Rechtsstreitigkeiten sowie konkrete M&A-Findings, die sonst über Kaufpreisabschlag, Escrow, Freistellung oder Holdback gelöst würden.

Die Contingent-Risk-Police wird um den konkreten Risikokern gebaut: versicherter Sachverhalt, Trigger, Schadenbegriff, Kostenpositionen, Verfahrensrechte und Ausschlüsse müssen denselben wirtschaftlichen Sachverhalt treffen. Anders als bei W&I gibt es keinen marktüblichen Garantiekatalog als Ausgangspunkt; jede Struktur wird einzelfallbezogen verhandelt.

Wer Versicherungsnehmer sein sollte, folgt der Risikotragung. Je nach Konstellation kommen Käufer, Verkäufer, Zielgesellschaft, Kläger, Beklagter, Anspruchsinhaber, Finanzierer oder Investor in Betracht. Vor einer Marktansprache ist daher zu klären, welches Risiko wirtschaftlich übertragen werden soll, welche Unterlagen den Risikokern tragen und ob eine Versicherungslösung gegenüber SPA-Regelung, Vergleich, Prozessstrategie oder anderer Spezialdeckung tatsächlich der richtige Weg ist.

W&I-Versicherung erfasst grundsätzlich unbekannte Risiken aus Garantieverletzungen im Unternehmenskaufvertrag. Wird ein konkretes Risiko in der Due Diligence identifiziert, offengelegt oder im SPA gesondert behandelt, ist es regelmäßig nicht oder nur sehr eingeschränkt über W&I versicherbar und wird häufig durch einen spezifischen Ausschluss ausgenommen. Für ein solches Risiko kommt innerhalb der Transaktion häufig eine Specific Indemnity in Betracht (siehe unten).

Tax Liability Insurance folgt einem ähnlichen Grundgedanken, wird aber wegen der spezialisierten steuerlichen Prüfung als eigenständige Produktlinie geführt. Bei nicht-steuerlichen Einzelrisiken richtet sich die Struktur nach dem Risikotyp: Anhängige oder konkret drohende Rechtsstreitigkeiten werden als Litigation Risk Insurance geprüft, Umwelt- und Eigentumsrisiken über entsprechende Spezialdeckungen, transaktionsgebundene Einzelrisiken über Specific Indemnity Insurance und sonstige bekannte Rechtsrisiken über den Contingent-Risk-Markt.

Insurers primarily assess the legal soundness of the risk position. They review the documented facts, the unresolved legal issue, possible counterarguments, and the calculation of the probability of occurrence and the amount of loss. A structured risk presentation is often sufficient for an initial assessment. A legal memo or comparable technical analysis is typically required for underwriting. In the case of litigation risks, additional factors include the status of the case, the stage of proceedings, cost risk, the risk of appeals, and enforceability.

An insurance solution is particularly worth considering when the facts of the case are documented, the outstanding legal issue can be described in a way that allows for review, the probability of occurrence and the amount of loss have been reasonably determined, and the insured event has not yet definitively occurred.

Risks for which the facts of the case are unclear cannot be insured, or can be insured only to a limited extent: for example, when the case essentially hinges on conflicting witness statements, technical questions of evidence, facts that have not yet been established, or a pattern of losses that is difficult to quantify. Such uncertainties can, at best, be mitigated through assumptions, conditions, sublimits, or exclusions.

The status of the proceedings also affects insurability. A loss that has already been definitively determined is no longer an open risk. As long as the insurance window is still open, the policy may be contingent upon an administrative decision, an initial claim, a court decision, an arbitration award, a decision on costs, a settlement with the insurer’s consent, or another specifically defined trigger.

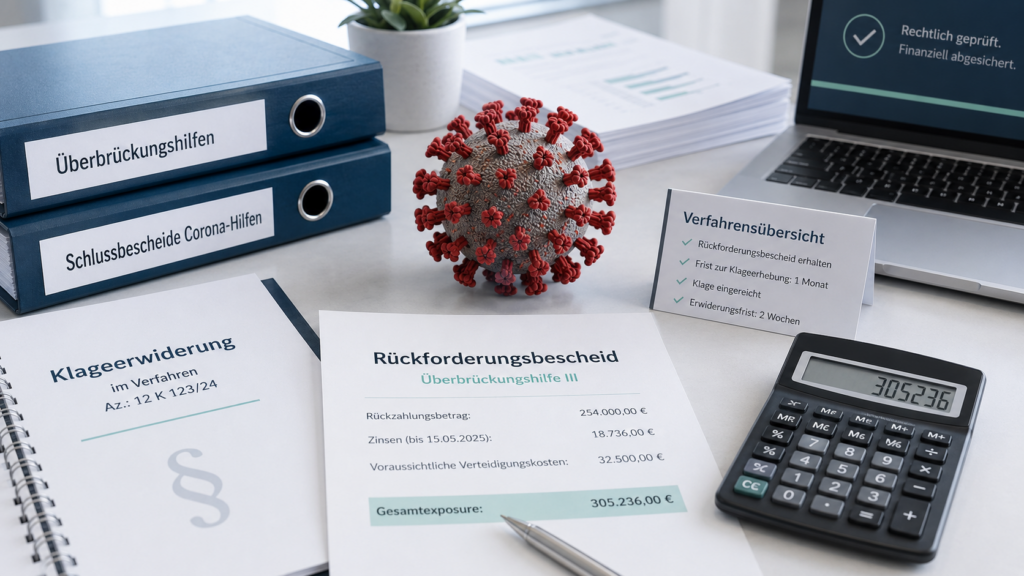

Unternehmen, die staatliche Förderprogramme in Anspruch genommen haben, können auch Jahre später mit Rückforderungsverfahren konfrontiert werden. Unser Team verfügt im Bereich Rückforderungsrisiken aus Corona-Wirtschaftshilfen über praktische Platzierungserfahrung mit spezialisierten Risikoträgern.

Identified risks can have a significant impact on the purchase price, liability provisions, escrow arrangements, indemnities, or closing security. A contingent risk policy—which, depending on the risk, may also be structured as a specific indemnity—can help remove such a risk from the negotiations if a purely contractual solution is not economically or tactically viable.

Litigation risk insurance may be worth considering if a legal proceeding affects the purchase price, financing, a balance sheet item, or the ability to attract new investors. Depending on the risk profile, this may involve litigation costs, the risk of an adverse outcome, the risk of appeals, or the enforceability of a judgment.

In restructuring or distressed M&A situations, potential liabilities, ongoing legal proceedings, or unresolved claims can significantly undermine transaction certainty and investor interest. An insurance solution can help quantify these risks and ease the burden of negotiations regarding the purchase price, liability, and financing.

In particular, risks arising from permits, licenses, recovery orders, or other administrative decisions may be insurable, provided that a verifiable legal analysis is available. Risks related to sanctions and fines require a separate legal review; often, the insurable aspect relates more to defense costs or certain non-penal financial consequences than to the fine itself.

Insurance can provide a basis for reassessing identified risk exposures vis-à-vis auditors, banks, investors, or acquirers. Whether this results in effects related to the balance sheet, financing, or valuation must be evaluated on a case-by-case basis with the respective advisors.

If a known risk becomes relevant to the transaction during due diligence or contract negotiations, the question arises as to how it should be allocated in the purchase agreement: through an indemnification by the seller, a purchase price deduction, an escrow arrangement, or a special warranty provision. Such a contractual solution typically binds the seller to the risk beyond the closing date and depends on the seller’s continued creditworthiness and willingness to pay.

Contingent risk insurance can protect, supplement, or economically replace this contractual allocation of risk; in this transaction-specific form, the solution is often structured as specific indemnity insurance. It can break a deadlock in negotiations, exempt the purchase price from a disputed deduction, and enable the seller to achieve a cleaner exit without ongoing liability.

In cases where proceedings are already underway or imminent, the focus is often not only on the proceedings themselves but also on their impact on the purchase price, financing, balance sheet, investor discussions, or negotiating position. Litigation risk insurance can help protect against a defined financial loss arising from the proceedings, an appeal, or the enforcement of a judgment.

The structure depends on which party bears the risk. For defendants, the risk of an unfavorable outcome is often the primary concern. For plaintiffs, the focus may be on litigation cost risks, securing a judgment already obtained, or the enforceability of a claim. In any case, insurers review the facts of the case, the prospects of success, the stage of the proceedings, the jurisdiction, the quality of the legal analysis, and the relationship between the premium, the coverage limit, and the remaining deductible.

Prozesskostenrisiken können ein Verfahren wirtschaftlich blockieren, auch wenn die eigene Rechtsposition vertretbar ist. Eine After-the-Event-Struktur deckt das gegnerische Kostenrisiko für den Fall des Unterliegens ab. Je nach Marktverfügbarkeit können auch eigene Kostenbestandteile oder Kostensicherheiten einbezogen werden; Umfang, Selbstbehalt und Kostenkontrolle werden fallbezogen verhandelt.

Für Beklagte kann ein laufendes Verfahren Kaufpreis, Finanzierung oder Bilanz erheblich belasten, selbst wenn die Verteidigungsposition gut begründet ist. Eine Adverse Judgment Insurance wird in der Marktpraxis vor allem für Beklagte geprüft. Auf Klägerseite wäre eine vergleichbare Absicherung problematisch, weil sie wirtschaftlich einer Garantie des Prozesserfolgs nahekäme. Die Adverse Judgment Insurance kann einen verhandelten Teil des wirtschaftlichen Risikos aus einer nachteiligen gerichtlichen oder schiedsgerichtlichen Entscheidung absichern, sofern die Verteidigungslinie belastbar dokumentiert ist und das verbleibende Restrisiko underwritingfähig bleibt.

Even if a plaintiff has already obtained a favorable judgment or arbitration award, the economic value of that claim is often not yet definitively secured. An appeal could reduce the awarded amount or nullify it entirely. Judgment preservation insurance can secure a negotiated portion of that value, thereby facilitating financing, settlement negotiations, or transaction valuation.

An awarded claim has economic value only if it is enforceable. In the case of judgments or arbitration awards against debtors in jurisdictions where enforcement is difficult, where the debtor’s financial situation is unclear, or where insolvency is imminent, enforceability itself can become an insurable risk. To this end, debtors, financial situations, enforcement jurisdictions, and legal barriers to enforcement must be thoroughly examined.

In arbitration proceedings, additional factors include confidentiality obligations, the rules of arbitration, the seat of the arbitral tribunal, and the enforceability of the arbitral award. Particularly in cross-border cases, enforcement remains a distinct risk factor depending on the state of enforcement, despite the New York Convention.

For contingent risk and litigation risk policies, the insured event must be precisely defined. Even minor discrepancies between the risk description, underwriting documents, and the policy language can determine, in the event of a claim, whether the risk intended from a financial perspective is actually covered.

In particular, the following should be reviewed:

Before making a recommendation, Risk Partners reviews these points in conjunction with the SPA, due diligence, the status of the proceedings, accounting, the financing structure, and the deal timeline, and determines early on what is insurable, what should be resolved contractually, and what cannot reasonably be presented to the market.

The policy format differs significantly from W&I insurance. While a relatively uniform market standard has emerged over the years for W&I insurance, each contingent risk or litigation risk policy is renegotiated specifically for the respective risk; a comparable degree of standardization does not yet exist in the market. This makes the placement process more complex and time-consuming; realistically, it takes several weeks, and in more complex cases, significantly longer.

An identified risk should be assessed for insurability at an early stage: for transactions, during the due diligence process; for standalone risks, as soon as the status of the proceedings, the exposure, and the available legal assessment are sufficiently clear. For litigation risks, additional factors to consider include the trial schedule, pleadings, court orders, expert opinions, settlement history, and cost budgets.

Before approaching the market, the risk assessment should be consistent; conflicting assessments from due diligence, internal memos, external opinions, and legal briefs can delay the underwriting process or reduce the chances of a successful placement.

| Parameters | Design |

| Policyholder | A company, investor, buyer, seller, plaintiff, defendant, or holder of an enforceable claim. |

| Insured Amount | Is based on the identified risk exposure, including potential defense costs, interest, incidental claims, and litigation costs. |

| Deductible | Depending on the risk and structure, coverage may be minimal, fixed in amount, or without a traditional deductible; for litigation risks, the policyholder often bears the financial risk. |

| Bonus | A one-time premium expressed as a percentage of the sum insured, depending in particular on the probability of occurrence, the amount of the loss, the term, the stage of proceedings, the jurisdiction, and the complexity of the risk. |

| Duration | Tailored to the scope of legal or procedural clarification; in the case of legal disputes, often until a final and binding resolution is reached or until a specific procedural milestone is reached. |

| Trigger | Depending on the risk; e.g., first-time claim, administrative order, contrary decision, court ruling, arbitration award, decision on costs, settlement with the insurer’s consent, reversal or reduction of a judgment on appeal. |

| Underwriting Basis | Legal or technical risk assessments, legal memos, pleadings, expert opinions, correspondence with government agencies, case history, cost budgets, and relevant transaction documents. |

| Scope of Application | In connection with a transaction or independently of a transaction; for known legal risks, administrative risks, regulatory risks, and litigation. |

For an initial assessment, we generally do not need complete underwriting documentation. The following information is helpful to start with:

Based on this, we assess whether it makes sense to approach the market, which insurers are suitable candidates, and whether contingent risk insurance (including its specialized forms, litigation risk insurance and specific indemnity), tax liability insurance, or a contractual solution is the more appropriate option.

This article is intended for general informational purposes only and does not constitute specific legal, tax, or insurance advice. Whether and to what extent insurance coverage is available depends on the specific facts of the case, a legal review, the insurers’ underwriting requirements, and the final terms of the policy.

How does Risk Partners provide support?

We are available on short notice to provide an initial assessment of the insurability, marketability, or structuring of a Contingent Risk & Litigation Risk Insurance policy.

Rufen Sie uns an unter der Nummer +49 160 92598958 oder schreiben Sie uns: dealinsurance@riskpartners.de.