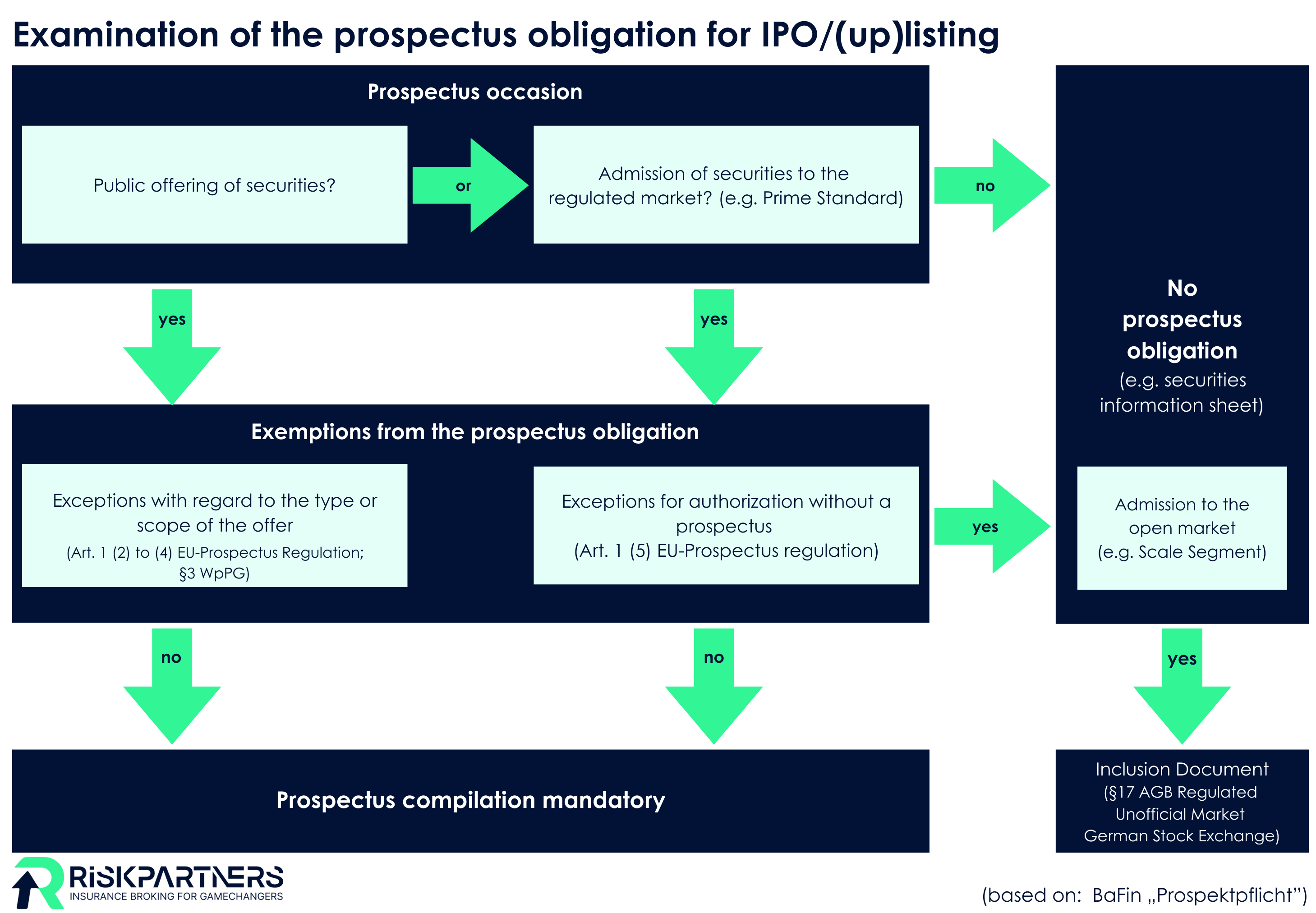

Risk Partners supports successful uplisting of Formycon AG to the Prime Standard

We warmly congratulate Formycon AG on its successful uplisting to the Prime Standard of the German Stock Exchange on November 12, 2024! Welcome to the Prime Standard league: A new champion of life sciences and biosimilars has successfully made the step from the scale segment. We proudly congratulate Enno Spillner, Dr. Caroline Redeker, Daniel Marquard and the entire team at Formycon AG on this great success and another important milestone on their way to