Being Public

Public prosecutor's office investigates: Suspicion of deception in short-time work (Sono Motors)

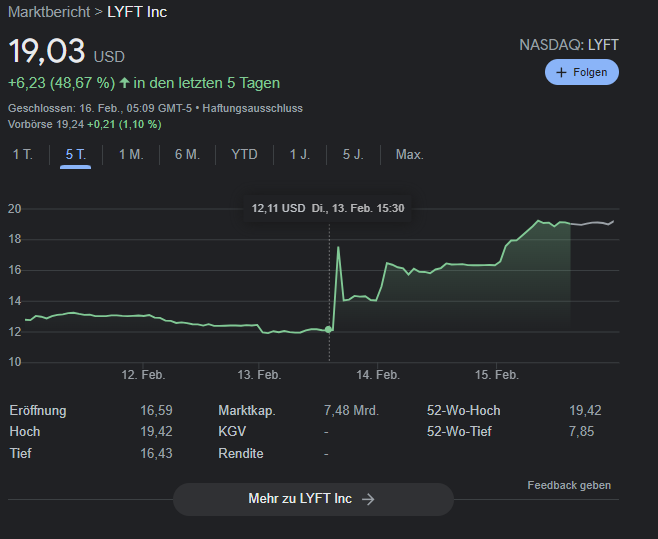

No startup bonus for criminal and administrative offenses. The incident and possible insurance cover. As exclusively researched by Hannah Schwär and her team at Capital Magazin, the founders of Sono Motors are now also facing problems with the public prosecutor's office. According to Capital Magazin, subsidy fraud in the context of short-time work and the programs surrounding the corona crisis is in the offing. The company, which is listed on the NASDAQ via De-SPAC, has already filed a report with the SEC. While the loss amount of EUR 40,000 is still being